Updated June 15, 2023

The Inflation Reduction Act has revolutionized the solar landscape for nonprofits in 2023. Discover how the new direct pay provision for the federal tax credit unlocks incentives that make solar an incredible financial benefit for your nonprofit. Say goodbye to hurdles and hello to financial and environmental benefits!

Everyone needs electricity, that’s just a fact. But if your nonprofit gets its electricity from the utility company, it’s a budget item that keeps on rising and will never go away. What if your organization could get its energy from the sun instead? Solar energy empowers nonprofits to use that budget allocation for their mission instead of their lights, computers, and air conditioning. It also increases your property value, reduces your carbon footprint, and models your values.

So why haven’t more nonprofits taken advantage of solar?

Traditionally, nonprofits have had a harder time going solar because, as tax-exempt organizations, they were not able to take advantage of the 30% federal tax credit, which makes solar projects more affordable. Here at Ipsun, we’ve worked with faith-based organizations to help them find creative ways to finance their projects, but we have also advocated for years for a Direct Pay option of the Federal Investment Tax Credit to make the process less complicated. Thankfully, direct pay for nonprofits became a reality through the Inflation Reduction Act of 2022.

The Inflation Reduction Act’s direct pay provision is a game-changer for nonprofits

The Inflation Reduction Act has unleashed not only an option to receive a cash refund of the 30%, but also increased the potential for a larger credit depending on the conditions of the project — potentially allowing up to 70% of the project’s cost to be refunded.

Better yet, it allows nonprofits to own their solar energy system, bringing other benefits of traditional solar incentives like Solar Renewable Energy Credits (SRECs), property tax exemption, various local incentives, and net metering credits. These benefits alone can add up to thousands of dollars in savings per month for a nonprofit, on top of the reduced cost of going solar brought about by the new direct pay option in the federal tax credit.

How does the direct pay option work?

Basically, the IRS will treat your nonprofit as if you did pay this tax, and you will get refunded the owed amount for your solar project.

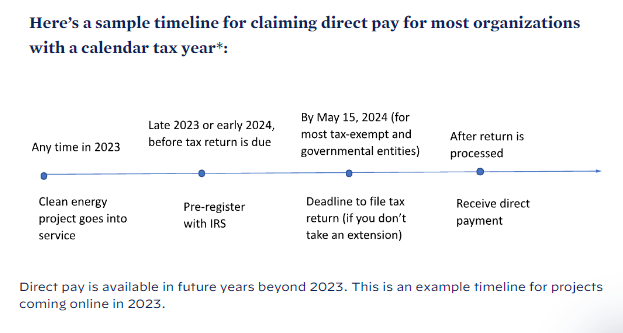

To receive the credit, you must make an election on a tax filing in the year in which the project is placed “in service,” meaning the system is able to be turned on and produce energy. Eligibility begins in 2023 and the solar project must be completed and capable of connecting to the grid before filing this tax credit election. You can read more about the specifics on the IRS website for the Inflation Reduction Act. And you can read more about how to file on the IRS website here.

New guidance for direct pay was released on June 14, 2023. You can read the overview from Whitehouse.gov here. In the adders section below, you’ll also find links to the most recent guidelines from the US Treasury Department and IRS. Further guidance will be released about pre-filing in late 2023. Here is an overview:

- Internal Revenue Code Section 6417 Tax credits can be monetized for projects placed in service after January 1, 2023 and before December 31, 2032.

- To receive this credit, make an election on a tax filing in the year in which the project is placed in service. Eligibility begins in 2023 and the solar project must be completed and capable of connecting to the grid before filing this election.

- Your organization will need to pre-file: You’ll need to register with the IRS and receive a registration number before you can file a tax return and receive payment. In general, each registration number corresponds to one clean energy property in one tax year—you will need to renew the number if you need to use it in other tax years.

- Once you receive your registration number, you’ll need to provide that and make the elective payment selection on your tax return (typically a Form 990-T for most entities that don’t normally file a tax return).

- Filing for direct payment must be completed by the end of the next tax deadline. May of the following year is the deadline for 501(c) non-profits.

- Allow up to one year or more to receive the direct payment.

- After 2024, Systems over 1 MW in size may receive a lower or higher direct pay percentage depending on domestic content and fair labor practices.

Who is eligible for direct payment through Section 6417?

Section 6417 allows an applicable entity to make an election to treat an applicable credit as a payment against federal income tax. An applicable entity means:

- Any organization exempt from federal income tax,

- Any state or political subdivision thereof,

- The Tennessee Valley Authority,

- Tribal or Native Entities,

- Any Alaska Native Corporation, or

- Any corporation operating on a cooperative basis engaged in furnishing electric energy to persons in rural areas

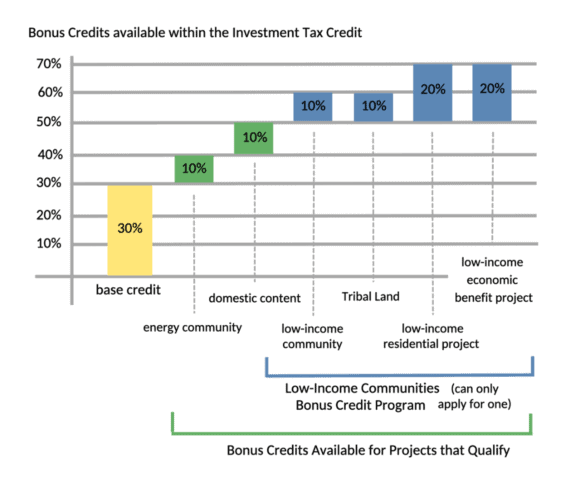

Added savings up to a total of 70% are available for nonprofits meeting environmental justice requirements

One of the most exciting provisions of the IRA’s direct payment option is the add-on percentages for environmental justice communities and US-manufactured equipment, allowing nonprofits to potentially receive 70% back on the cost of their project.

Nonprofits can qualify for the extra adders if the following conditions are met. Follow the links to find the latest IRS Guidance on each.

Energy Community Adder: An extra 10% is added to the tax credit if the system is installed on a brownfield site or community with coal plant closures. The US Department of Energy has created a map displaying data for qualifying energy communities including:

- 1) Census tract with a coal closure,

- 2) Census tract directly adjoining a census tract with a coal closure, or

- 3) Areas that meet the Fossil Fuel Employment (FFE) threshold of 0.17% (energy community status not yet assessed).

- 4) Brownfields are not shown on the map, but do qualify.

Here’s the PDF on the most recent guidance, issued June 15, 2023: Notice 2023-45

Domestic Content Adder: An extra 10% is added to the tax credit if the system uses domestically manufactured equipment. To meet the domestic content bonus criteria, taxpayers must construct a project with 100% U.S. content steel and iron and incorporate the appropriate “adjusted percentage” of domestically manufactured products.

The adjusted percentages of domestic content for manufactured products on projects larger than 1MW are as follows:

- 40% for projects that begin construction prior to Jan. 1, 2025;

- 45% for projects that begin construction after Dec. 31, 2024, but before Jan. 1, 2026;

- 50% for projects that begin construction after Dec. 31, 2025, but before Jan. 1, 2027; and

- 55% for projects that begin construction after Dec. 31, 2026.

Low-Income or Tribal Community Bonus Program: An extra 10-20% is added to the tax credit if the system is installed in a low-income area or tribal land. This program is on an application basis. Currently, projects can only apply for one of the four bonus credits within the Low-Income Communities Bonus Credit Program. This means a project could either receive a 10% or 20% bonus credit, depending on their eligibility. This program is still waiting on more guidance, but here are a few more details:

- The Department of Energy (DOE) will accept applications for the Low-Income Communities Bonus Credit Program in the third quarter of 2023.

- Eligible projects must apply for the adder before the project is installed and ‘placed in service’ (Section 4.05; defined in Section 2.06 of the IRS’ guidance).

- The application for the two 20% adders will be open for 60-days in Quarter 3 of 2023; the application for the two 10% adders will be available for 60-days later in the year (Section 4.07).

- The IRS will release more guidance before the application windows begin.

Updates to the guidance will be posted on the WhiteHouse.gov IRA fact sheet here and on the IRS website here.

There’s never been a better time for nonprofits to benefit from solar energy

Nonprofits, churches, and synagogues now have unprecedented access to solar incentives in 2023. Thanks to the Direct Pay provision and additional adders, tax-exempt organizations can invest in solar energy with ease. Seize the opportunity and join the sustainable energy revolution today!

Be sure to consult a tax professional to ensure you have the most recent guidance on this new tax regime. As you know, we’re solar professionals, not tax professionals!

Questions?

Reach out to us any time with questions or ideas about how your favorite nonprofit can take advantage of these great new incentives. We’d love to talk about how we can help your organization save money and save the planet! Give us a call at 703-249-6594 or click below to get in touch!